Gold Really Does Rise Overnight. We Couldn't Keep a Cent of It.

The 'London bias' says gold's gains accrue between the PM and AM fixes. We measured it on raw tick data and it's there: +$0.90 per ounce per night. Then we tried to trade it, and the nightly costs came to $1.47.

There is a decades-old claim about gold, popular in corners of the internet that believe the price is managed: the metal rises overnight and stalls or falls during the London and New York day. Strip away the conspiracy framing and a measurable statement remains. Buy at the London PM fix (3pm local), sell at the next morning's AM fix (10:30am), and you should capture most of gold's long-run appreciation while skipping the day session entirely. A 54-year decomposition of the fix data supports the pattern, and academic work found systematic downward pressure into the PM fix through the 2004-2013 era that later fed the fix-manipulation lawsuits.

We specced it as a residue test, the same framing as our London fix study: the strongest evidence predates the 2015 reform of the fixing process, our data starts in 2019, and rejection was an acceptable outcome from day one.

The claim survives measurement

Before trusting any tester output, we measured the raw effect straight from the M1 file, no stops, no sizing, no strategy. From 2019 through 2021, the overnight leg (PM fix to next AM fix) gained $692.72 per ounce across 774 nights. That is $0.90 a night at a 54.5% win rate. Gold rose $536 in total over the same window, which means the overnight leg carried more than all of the metal's appreciation, exactly as the London-bias claim says. The anomaly is real, and it is not small.

So we built the EA and smoke-tested it: entries at the PM fix to the minute, clock exits at the next AM fix (weekend holds carry to Monday's), native swap charged on every night held. The machinery worked.

The arithmetic does not

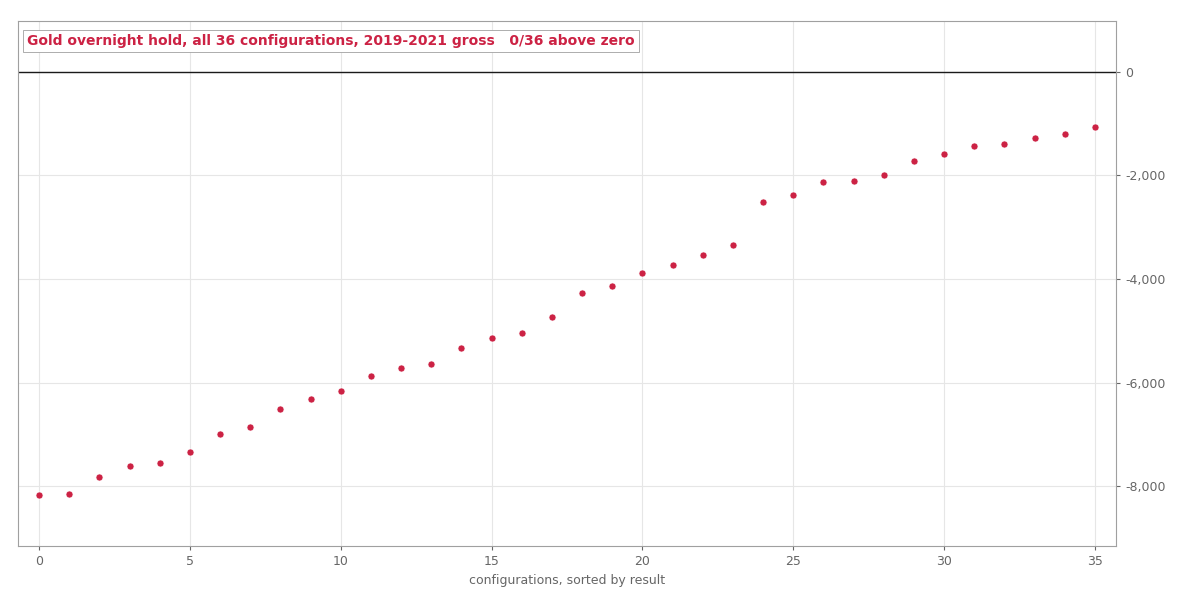

All 36 configurations lost money, across two full grids. Stops from 2x to 4x hourly ATR: best cell minus $4,727, worst minus $8,171. We widened the stops to genuinely disaster-grade 6x to 12x and the best cell improved to minus $1,065, converging toward zero from below and never crossing it.

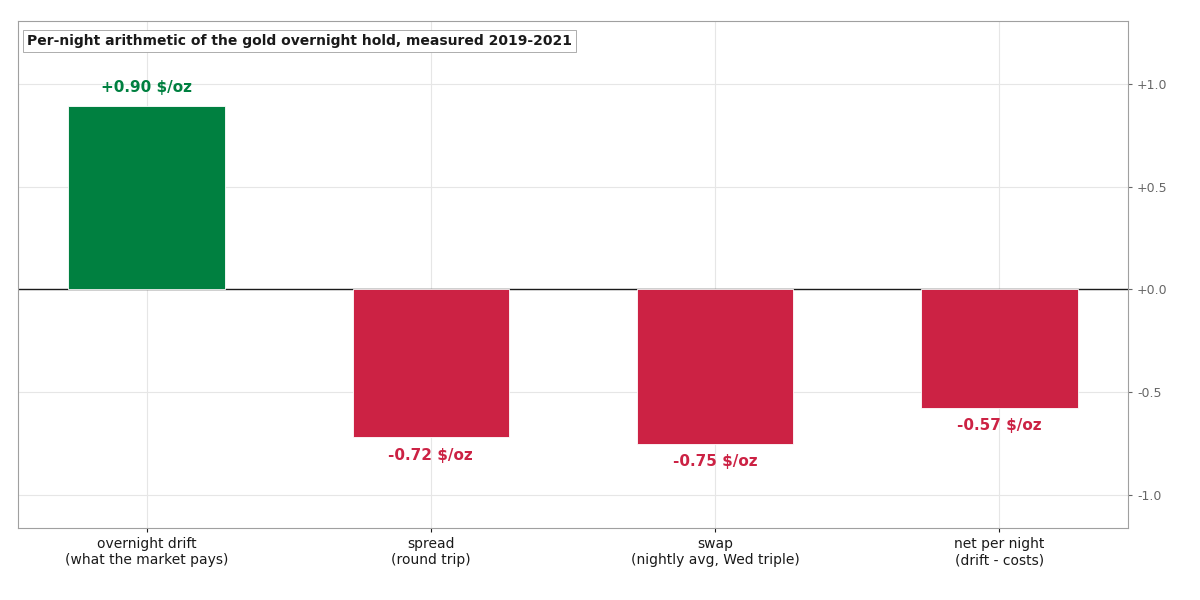

The per-night arithmetic: the drift is real and the costs are bigger

The per-night arithmetic: the drift is real and the costs are bigger

The chart above is the whole autopsy. The market pays the overnight holder $0.90 an ounce. Collecting it through a CFD costs $0.72 of spread per round trip, plus swap. Our tester charges gold's real financing natively: $62.60 per lot per night on the long side, tripled on Wednesdays, which averages out near $0.75 an ounce. Costs of roughly $1.47 against a drift of $0.90. No stop width, entry offset, or Friday filter changes that subtraction, and every one of the 36 cells was doomed before it ran.

All 36 configurations, gross, 2019-2021: nothing above zero

All 36 configurations, gross, 2019-2021: nothing above zero

There was a second, quieter problem. Split by year, the drift was $0.94 a night in 2019 and $1.74 in 2020. In 2021 it was $0.002. The pattern that built the 54-year statistics faded to nothing inside our own in-sample window, so even a costless version would have had nothing left to harvest by the end.

The mirror image of the triple swap

Readers of our Wednesday triple-swap study will recognize the shape. There, the carry was real and arrived to the cent while the price leg destroyed the account. Here, the price drift is real and measurable while the carry, now on the paying side, destroys the trade. Both studies end at the same rule, which is now written into our research priors: any strategy that holds overnight by design must clear the spread AND the financing, measured, before anything else about it matters.

The strategy consumed zero out-of-sample runs. The 2022-2026 window stays clean, and the $692 the market really did pay overnight holders in 2019-2021 stays where it always was: on the other side of the costs.

All tested strategies, winners and losers, live on the results page.

Past performance is not indicative of future results. These are backtests with realistic cost assumptions, not live trading records.