We Transferred an Academic Momentum Effect to EURUSD. The Market's Most Efficient Pair Said No.

Intraday time-series momentum is documented in equities and RUB-USD. On post-2019 EURUSD, the best of 48 configurations made $371 in three years. A clean transfer-test failure, with costs ruled out.

Intraday time-series momentum has a respectable paper trail: the first half-hour predicts the last half-hour in US equities (Gao, Han, Li, Zhou), the effect shows up across global markets, and in FX it was documented on RUB-USD tick data by Elaut, Frommel and Lampaert in the Journal of Financial Markets. The proposed mechanism is structural rather than magical: liquidity providers hate holding inventory overnight, so late-session flows lean the same way the day has been leaning.

We wanted to know whether any of that survives on a major pair. So we specced the standard practitioner translation: measure the move from the day's open by a fixed morning hour (04:00 to 10:00 UTC tested); if it exceeds a threshold (10 to 40 pips), ride that direction until a hard 21:00 UTC exit; never hold overnight, because the mechanism itself says overnight is what everyone is avoiding. EURUSD was chosen deliberately: at 0.1 to 0.3 pips of spread against 10-to-40-pip targets, this is the one test in our registry where costs could not possibly be the killer. The spec flagged it honestly as a transfer test: the literature's FX evidence comes from an exotic pair a decade ago.

The grid came back empty

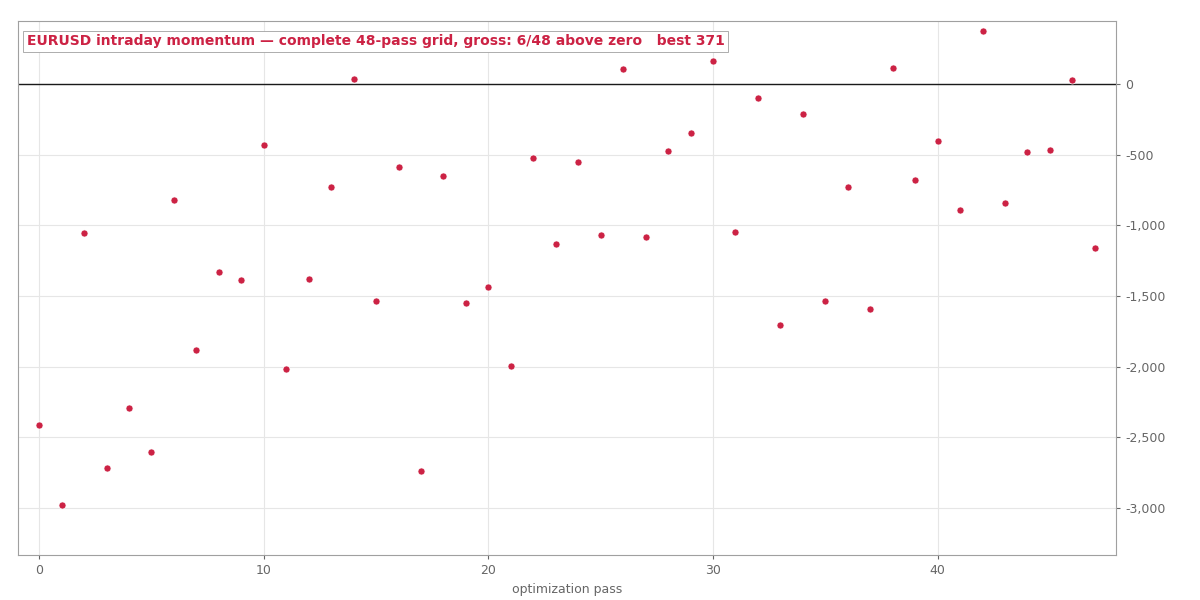

All 48 configurations, gross, 2019 to 2022. Six finished above zero; the best made $371 in three years.

All 48 configurations, gross, 2019 to 2022. Six finished above zero; the best made $371 in three years.

Forty-eight combinations over 2019 to 2022. Six finished above zero, all clustered at the 08:00 signal hour, and the best earned $371 over three years on a $10,000 account: a profit factor of 1.09 against our 1.3 validation bar. Worse, the two gates a candidate needs could not be satisfied at the same time anywhere in the grid: every configuration with enough trades to be statistically meaningful (150-plus) sat at or below breakeven, and every profitable configuration traded too rarely (56 to 125 times). No parameter plateau existed.

We rejected it at the in-sample stage without touching the out-of-sample window. Could more iteration have polished PF 1.09 into something higher? Probably a little, and that is exactly why we stopped: tuning a flat signal until it clears a bar would just manufacture a validation.

Why this negative is worth having

The mechanics were airtight: the smoke test showed entries at 06:00 sharp, hard exits at exactly 21:00:00, one trade a day, risk capped as specified. The signal is what failed, and it failed with costs ruled out. That makes this the cleanest kind of negative result: the day-open-anchored morning move simply carries no information about the rest of the day on post-2019 EURUSD at any threshold we tested.

Which, on reflection, is what the literature itself hints at. The effect's documented homes are markets with structural friction: equity closing auctions, an exotic currency pair during a crisis decade. EURUSD is the most efficient, most arbitraged, cheapest-to-trade instrument on the planet. Wherever intraday momentum still lives, it is not there. Our momentum family now has its first data point, and it points away from the majors.